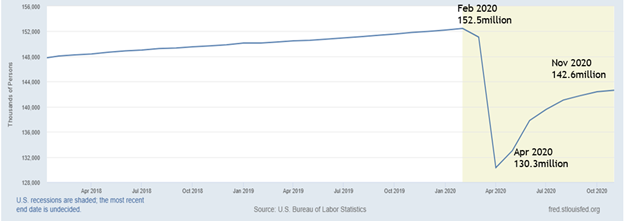

Nearly a year after the initial COVID-19 outbreak, its full impact on the US economy remains unclear. Several economic indicators conflict with each other- with some of the largest corporations in the world reporting record profits, while nearly ten million more Americans are now unemployed than when they were at the start of the year.

U.S. Non-Farm Payroll

Additionally, what is trending in the opposite direction is that more than four million Americans left the workforce entirely since February to November 2020 as measured by the US labor force participation rate. Labor force participation declined from 63.40% to 61.50% during that period as workers were discouraged or voluntarily stayed out of the labor force. Such developments could have long-term impacts on the unemployed’ s earnings potential which could lead to more adverse ramifications down the road. A weaker labor force participation rate could also dampen the pace of a potential economic recovery with additional slack in the labor market mitigating recovery efforts.

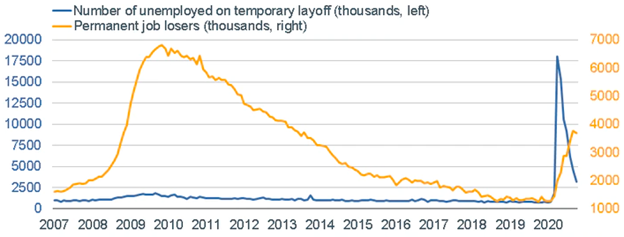

Despite the US economy adding nearly 13 million jobs since the trough of the recession, a subset of the unemployed have been unable to find a job despite actively searching. The share of long-term unemployed workers who have been unemployed for more than 27 weeks now make up close to 37% of the unemployed pool. The longer this persists, we could potentially see labor force participation rate dip further as the unemployed become discouraged workers. We expect the trajectory of the labor market to remain volatile in the near term as cities and states reverted to its shelter-in-place order in the last few weeks of 2020. However, the prospects of a wide vaccine distribution and additional stimulus package could help offset some of the inflicted damage.

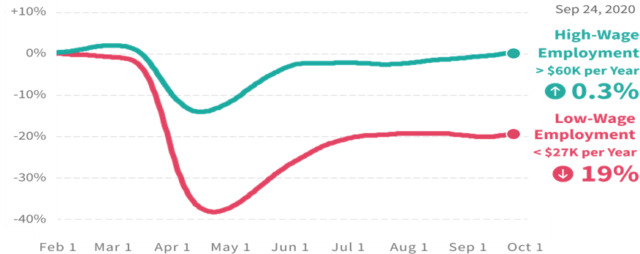

On the flip side, housing and retail sales posted strong numbers in 2020- supported by record low mortgage rates and a thriving upper middle class in the US. The employment picture between high wage and low wage workers highlights the uneven and divergent impact COVID-19 has had on our economy. The employment recession for high wage earners ended at the end of September when job additions returned to positive territory for the year. Conversely, low wage employment continues to remain below pre-crisis levels driven by business restrictions and disruptions.

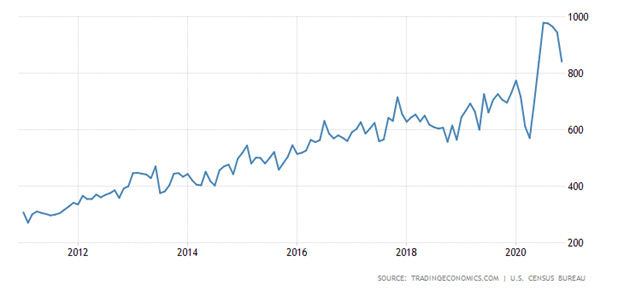

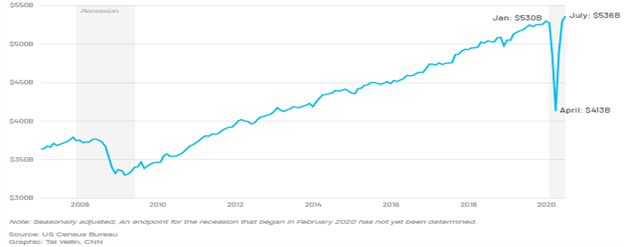

Despite slowing home sales in the last few months of the year, the US housing market was also a bright spot in the economy in 2020. US existing and new home sales reached its highest level since December 2006.

U.S. Existing Home Sales

Record low mortgage rates coupled with shifting living preferences during the pandemic powered the housing market. A healthy housing market boosted demand for newly built housing which could spur more hiring and spending by homebuilders. Increased home sales can also lead to higher consumer spending on appliances, furniture, and other home goods- all positively contributing to higher economic growth.

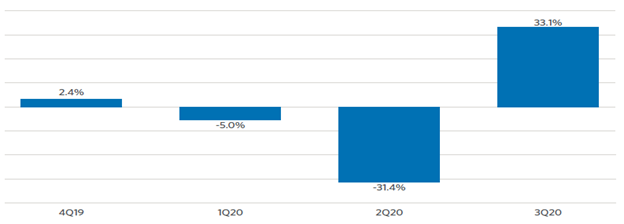

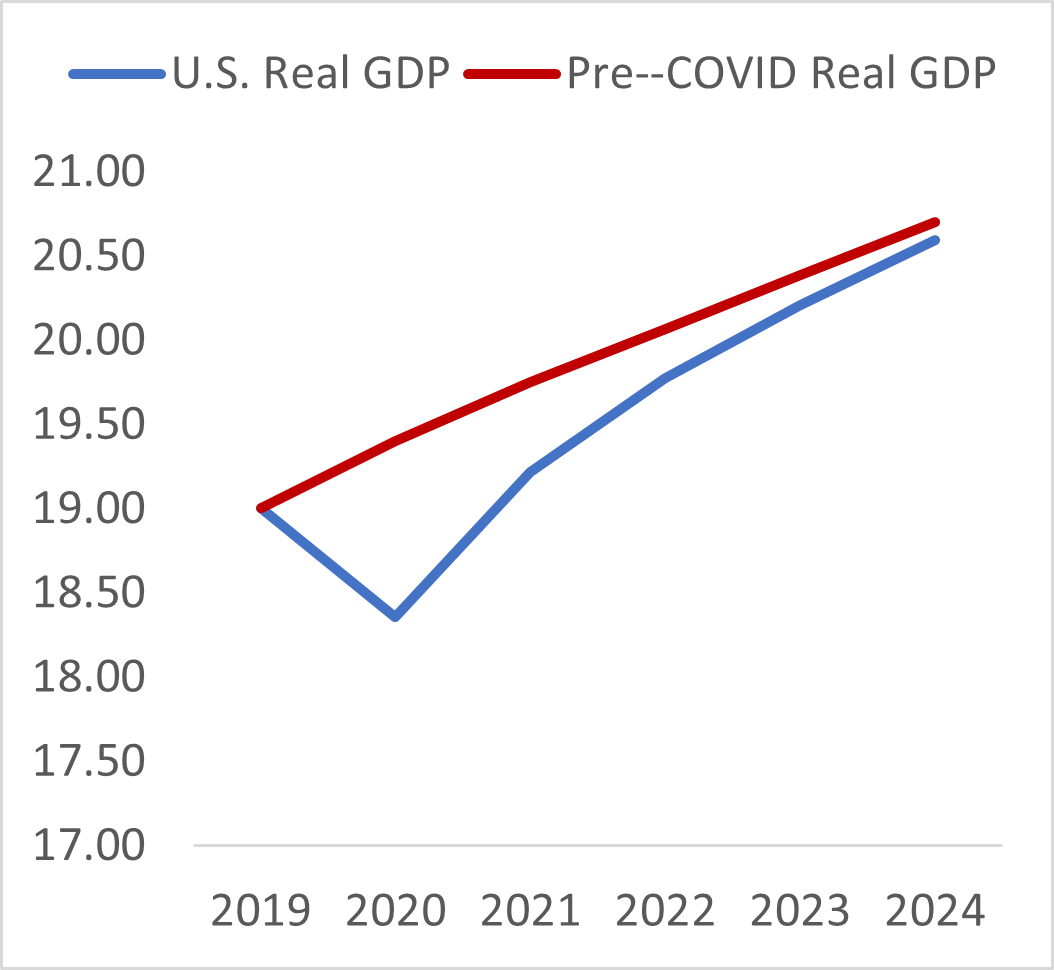

US economic growth as measured by GDP experienced an unprecedented variance in Q2 and Q3 2020.

U.S. GDP Growth (4Q19-3Q20)

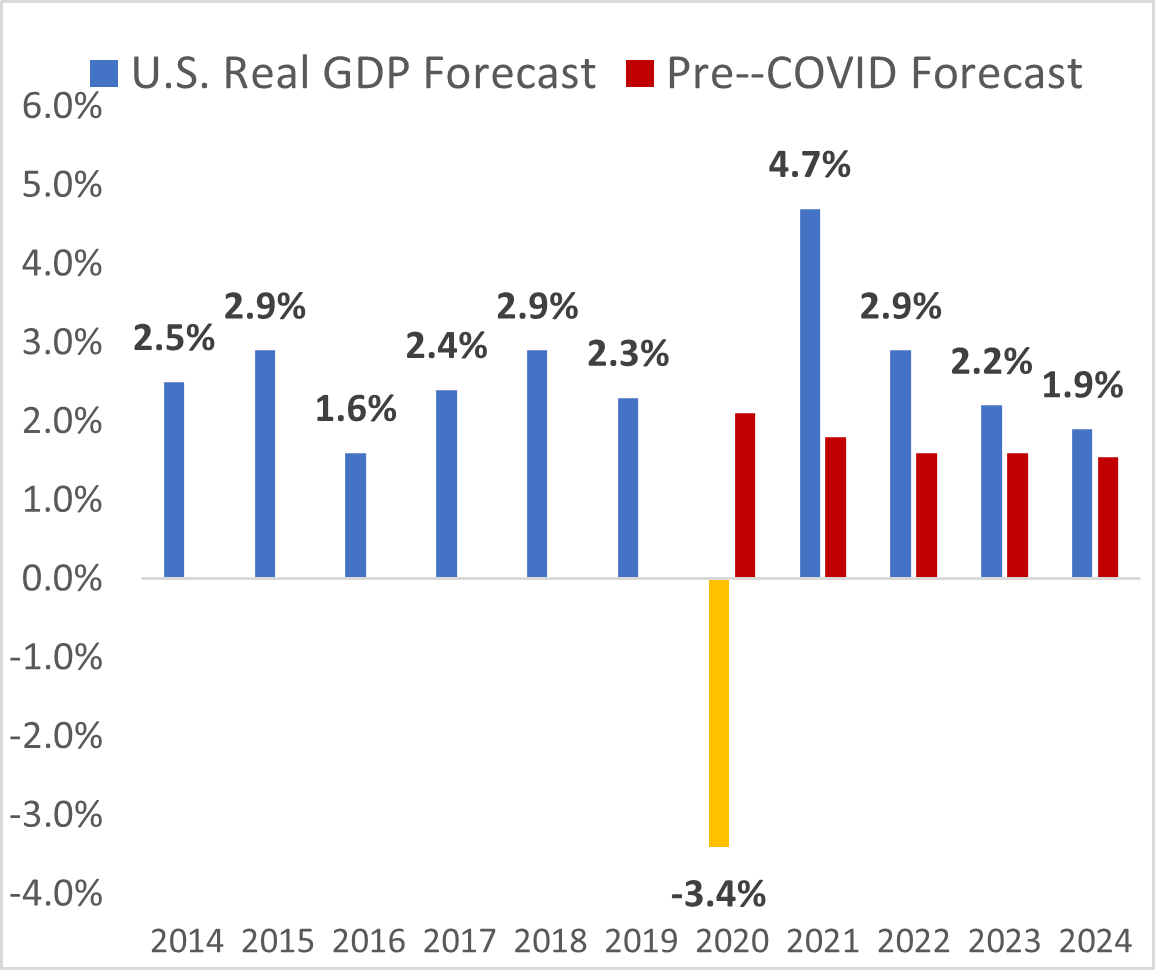

After what was marked as the worst quarterly GDP print since the Great Depression in 2Q2020 with an annualized growth of -31.4%, the economy came roaring back in 3Q2020 with an annualized growth of +33.1%, the best in history. Such large variance was the epitome of the adverse impact lockdowns had on the general economy to help stop the spread of the virus. The dramatic turnaround in the third quarter created a renewed sense of optimism among consumers and investors. Experts were forecasting GDP levels not to return to its pre-COVID levels in 2019 until the end of 2022 and beginning of 2023. However, after the blowout 3Q GDP performance, GDP levels have been moved up considerably, with experts forecasting GDP to return to pre-crisis levels at the end of 2021. This move up the timetable was viewed favorably by the markets

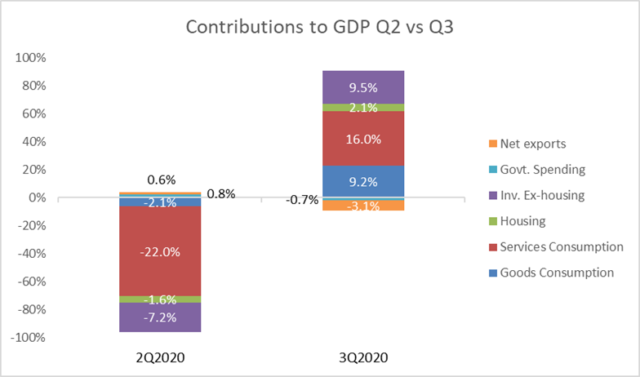

Looking at the major contributors to GDP over the course of those two volatile quarters, we can observe that the bulk of the decline in the second quarter was driven by the decline in consumption, primarily services consumption as service-based businesses were forced to shut down. The silver lining in the second quarter were government spending and net exports due to an increasing in government spending catalyzed by the $3 trillion stimulus package. Net exports also contributed positively to GDP with global trade severely disrupted, helping the US economy which is traditionally a net importer become a net exporter in the second quarter.

As the economy began to re-open in the summer into the fall, growth was observed across the board, led by services and goods consumption which together added 25% of growth to the GDP print and was aided by the stimulus package. The consumption comeback was so profound that by the end of July, retail sales were back up to pre-crisis levels, highlighting the resiliency and significance of the American consumer. With consumption making up close to two-thirds of US GDP, the health of the consumer remains paramount in any recovery efforts moving forward.

Advance Monthly Sales for Retail and Food Services

Looking ahead, 4Q2020 and 1Q2021 GDP are likely to experience some headwinds due to the surging COVID-19 cases and new rounds of business shutdowns. Strong job additions since the bottom of the crisis are also starting to abate, highlighting the very fluid nature of this crisis. However, when looking into the second half of 2021, brighter prospects could begin to emerge as vaccine accessibility drives looser business restrictions and pent-up demand from consumers and businesses along with fiscal stimulus working its way through the system all contributing to a potential robust economic recovery.

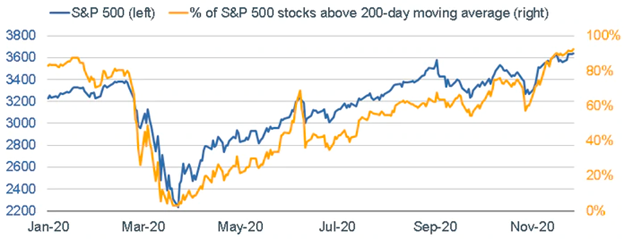

In our previous quarterly commentary, we postulated that the sustainability of the equity market recovery rests heavily on the other segments of the market to pull its weight- given that the market recovery at that time was led by a handful of technology stocks. Fast forward three months and that narrative played out almost according to script- with a broad rotation from technology stocks into more economic-sensitive sectors of the market. As a result, the S&P 500 experienced broader upside participation among its index constituents, fueling the momentum further.

Part of the reason behind the favorable market reaction in the fourth quarter, especially in November and December can be partly attributed to the outcomes of the presidential and congressional elections. Predominant market fears of the election preceding November appeared to be less significant than previously thought with fears of a blue wave scenario and uncertainties over a contentious election appear not to have come to fruition. Although there are possibilities that the Democrats could flip the Senate with two run-off elections in Georgia on January 5th which would result in the Democrats controlling both the White House and Congress, the margin of error for majority votes even if Democrats controlled both the White House and Congress remain relatively slim, lowering the prospects of the more progressive Democratic plans from being passed.

As the results of the general election started to trickle in, another major milestone in the COVID-19 development was achieved- with Phase 3 initial vaccine data from Pfizer and BioNTech, showing a 95% efficacy rate in 94 vaccinated patients, far surpassing the FDA’s hurdle rate for approval. Clearer skies from the general election coupled with strong initial vaccine data helped propel the market to newer heights, creating optimism among consumers and investors and fueling the rotation into more economic sensitive sectors.

Financial markets also benefited from strong corporate earnings showing in the quarter. According to Factset data, 84% of S&P 500 companies reported positive earnings per share surprises, with an average positive earnings surprise of 19.5% above estimates. This marked the highest percentage of companies beating their earnings estimates and beating them with by the second highest margin of 19.5% since Factset began tracking the data.

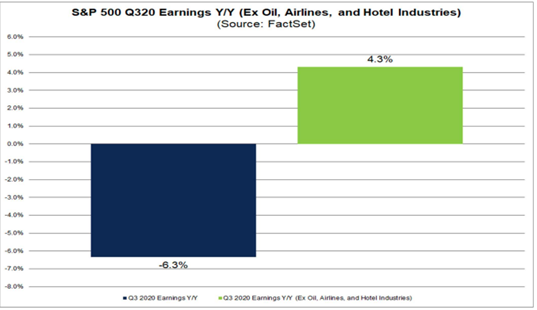

In aggregate, the average blended earnings for Q32020 was a decline of -6.3% despite more industries (36 out of 63 industries) reporting year over year earnings growth. This exemplifies the very harsh and uneven nature of Covid-19’s impact on different industries. Three industries had an unusually significant year over year earnings decline that contributed to most of the earnings decline in the S&P 500. Those three industries were Oil, Gas, & Consumables, Hotel, Restaurants & Leisure, and the Airlines/Travel industries, three of which were the most severely impacted by Covid-19. When excluding these three industries, the S&P 500 would have recorded a 4.3% earnings growth year over year, highlighting a healthier corporate environment than what the headline number may suggest.

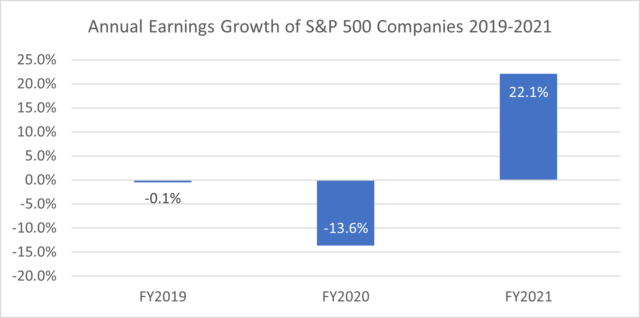

Looking ahead into fiscal year 2021, Factset Earnings Insights estimates that S&P 500 operating earnings per share for FY2021 to be approximately $170 per share, representing a 22% increase from 2020 but more importantly, bringing earnings per share back above pre-crisis levels with EPS standing at $163 in FY2019. Although the road to 22% earnings growth in FY2021 is subject to momentum in consumer spending, business re-opening, handling the virus, and fiscal stimulus impact, these factors seem to be recognized by consensus, which we expect momentum to pick up in the second half of 2021.

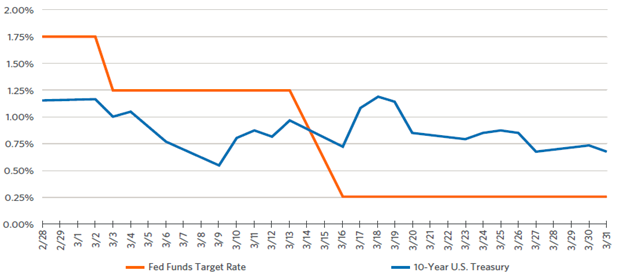

The Federal Reserve unprecedented actions during the early onset of the virus outbreak proved crucial in the market and economic recovery. The move from 1.75% to zero in sixteen days during the first half of March was just the beginning. The Fed also re-implemented its large-scale open market asset purchases, also known as “quantitative easing,” designed to restore confidence and liquidity in bond and equity markets.

Fed Funds Rate & 10-Year Treasury

Investment Grade and High Yield Spreads

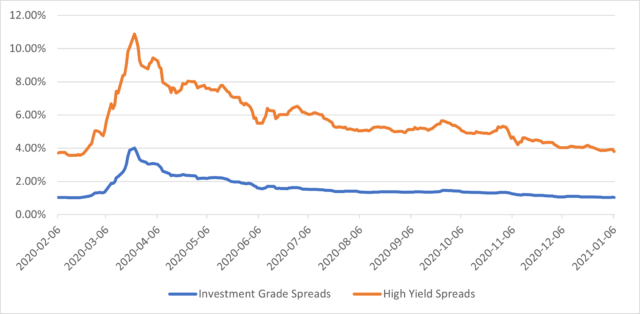

The consequence of its ongoing monthly purchases of $120 billion of Treasury bonds and MBS resulted in a swift tightening of credit spreads after they widened considerably during the height of the outbreak. Spread differential versus comparable maturity Treasuries were cut by more than half in the ensuing months after nearly tripling in a matter of weeks during the height of the outbreak. The Fed’s strong action provided significant support for a functioning credit market that allowed liquidity to flow through businesses and households during a tough environment. The cost of their actions resulted in essentially doubling their balance sheet from $3.7 trillion to $7.3 trillion as of the end of December.

Signs of shifting Federal Reserve policy were also observed after the Fed’s symposium in August whereby Fed Chairman Jerome Powell announced a “long run inflation targeting” approach, a small but significant move away from its 2% inflation targeting approach. The “long-run inflation targeting” approach focuses more on symmetrical analyses on inflation, permitting a higher tolerance for inflation to run above the Fed’s long-term inflation target of 2% for sustained periods before taking actions to combat it. Additionally, in the same announcement, Chairman Powell also verbalized an adjustment to their approach on employment trends relative to interest rates. Prior to the virus-induced recession, inflation has been staying along multiyear lows despite low unemployment bringing the “Phillips Curve effect” into question. The Fed now seems content on letting full employment run for sustained periods before taking pre-emptive monetary actions to curb inflation due to a tighter labor market.

Looking ahead, both developments represent a significant change in inflation and employment perspectives at the Fed and presents a reasonable case that we might not see rate hikes from the Federal Reserve for some time, supporting a case for a lower-for-longer interest rate environment which are supportive of risk assets for the long run.

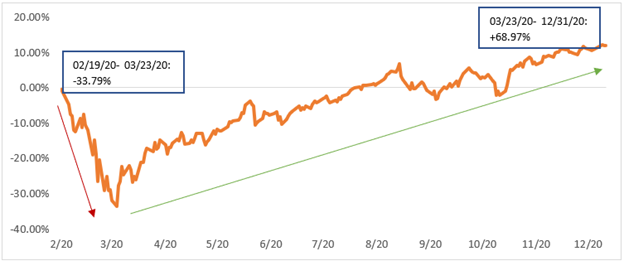

From the stock market’s perspective, 2020 was a year of two markets. The first three months of the year experienced unprecedented upheaval driven by a virus-induced contraction while the next nine months of the year manufactured one of the best market rallies in recent years.

S&P 500 Total Return (Feb. 19 – Dec. 31, 2020)

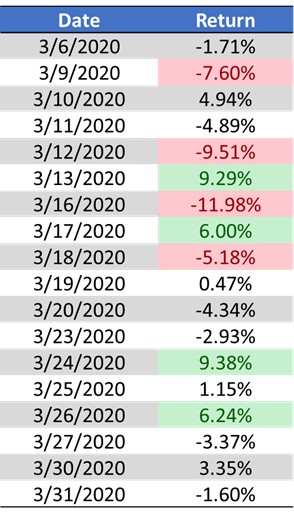

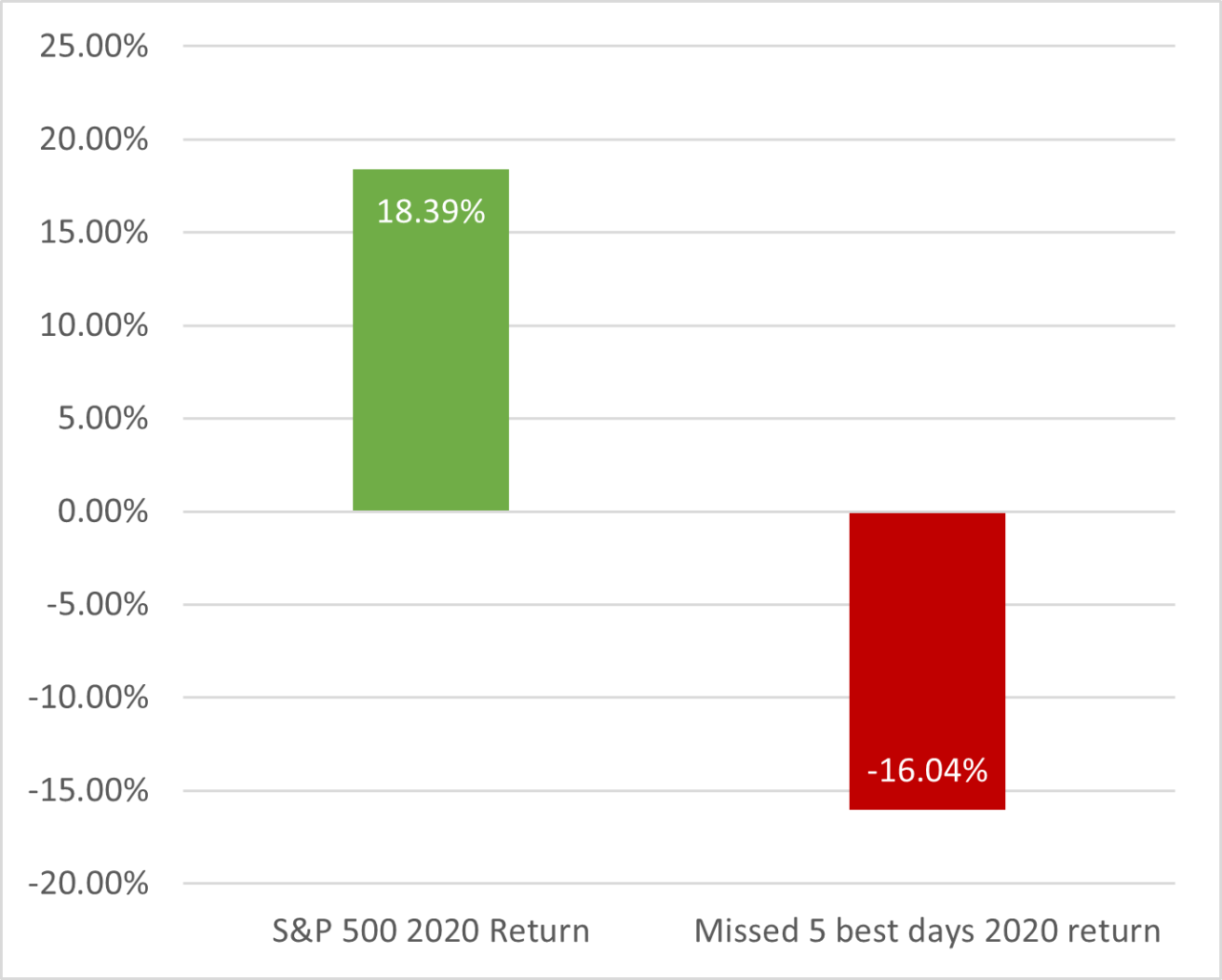

From a psychological perspective, it took tremendous courage, patience, and perseverance for investors to remain invested throughout the year and achieve the headline market (S&P 500) return of 18.39%. Had investors missed just the 5 best days in the market, their returns would been a meager -16.04% for the year. What is particularly challenging in timing the market is that the best and worst days are usually days if not weeks apart. Using 2020 market events as an example, the best and worst days of the market were within a 2-week timespan of one another. Between March 12 to March 18, the markets were gyrating between its worst and best days of the year.