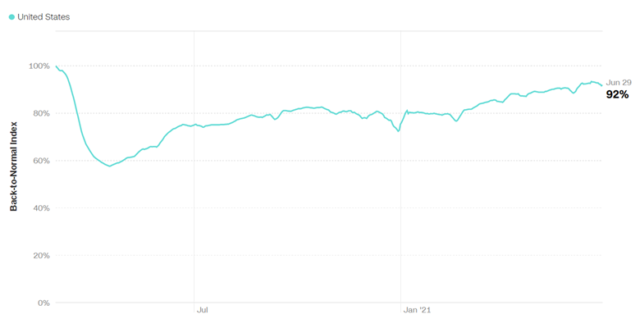

The stock market has all but surpassed its pre-pandemic level high, setting numerous records in the second quarter of 2021. This is driven in part by a healthy trend for corporate earnings, $5 trillion of additional fiscal stimulus circulating the economy, and improving fundamental economic backdrop. Some segments of the economy are running at levels above its pre-pandemic high (eg: retail sales, personal savings, housing), while other segments have dramatically improved since the bottom of the economy in Q2 of last year (industrial production, employments, recreational activities). According to the “back-to-normal” index created by Moody’s Analytics, the economy in the United States is operating at 92% of where it was in early March 2020, with significant improvements in Q2 2021 as the economy continues to re-open and a larger percentage of the population are getting vaccinated. What we find useful in this index is that it goes beyond the typical measures used to judge how the economy is doing such as GDP and employment. It combines 37 national and state level indicators ranging from industrial production to OpenTable restaurant bookings to provide a better understanding of how businesses and consumers are responding to the pandemic recovery.

This has been an incredible recovery and we anticipate further gains to be realized as vaccination programs continue to be rolled out globally. Here in the United States, a strong corporate environment and a healthy consumer supported by high personal savings rates are catalysts to stronger demand in the second half of the year as the economy continues to re-open.

With that brighter outlook, COVID-19 market concerns appear to have taken the back seat while a new series of market concerns are starting to build. Although we encourage investors not to discount lingering COVID-19 risks, this commentary will be focused on addressing the new series of market concerns. Today, there are three main themes that emerge when observing marketplace behavior. These include anxiety over inflation risks, market valuations, and potentially higher taxes on the horizon.

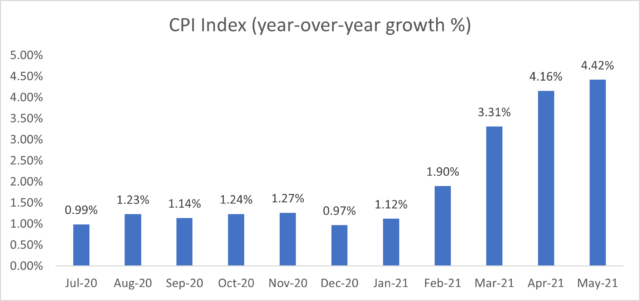

We are now experiencing inflation rates not seen in decades- May CPI numbers indicate a year-over-year inflation rate of 4.5% (highest since 2008) and core CPI which excludes food and energy prices came in at 3.8% (highest since 1992). Major inflation momentum is seen in the price development of major commodities such as copper, oil, and steel- all of which have doubled since their low in 2020. Additionally, worker shortages in the services industry are also contributing to some upward inflationary pressures.

We believe the current inflationary environment is driven primarily by a combination of three forces- reflation stage in the business cycle (cyclical), shock to global supply chains (unique event), and base effects of weak prices from a year ago (cyclical). Firstly, the economy is growing back up to its longer-term trend, following a dip in the business cycle due to the pandemic. We refer to this stage as the reflation period where growth and inflation trends usually run above the long-term average as the economy recovers from the trough of a business cycle. What is extraordinary with this reflation cycle though is the pace in which the economy recovered from the depths of the recession. Despite the black swan nature of the pandemic, the capital stock of the economy and aggregate consumption activity remained intact, all things considered, with the help of unprecedented policies. This resulted in a swift catch-up effect in consumption demand as the economy re-opened, that fueled the rise of the reflation cycle.

The one-off effect of increased demand did not translate to the supply side which has yet to return to pre-pandemic levels. Increased factory lead times due to challenges in global supply chains are causing shortages which leads to anxiety among businesses and consumers. Such anxiety could lead to increased stockpiling behaviors which in turn could result in sustained higher inflation. Although stockpiling behaviors are not widely prevalent today, it is a development that bears watching for potential short-term sustained inflationary risks. Nonetheless, this supply chain issue that was created due to a one-time event (pandemic) appears manageable as time progresses.

Recent inflation data can also be clouded by base effects of weak prices from a year ago. When we observe the inflation jump between February 2021 to March 2021, the jump coincides with the start of the disinflationary period the economy experienced a year ago. The higher inflation figures in the subsequent months are also affected by these base effects. We expect year-over-year inflation pressures to be less clouded in the second half of the year, which will become a more accurate depiction of actual inflation.

We view that the current above average inflation period is likely to be transitory. Firstly, inflation contains a self-defeating concept given that inflation tends to fix inflation. Take the housing market for example where sustained high prices would price out potential buyers which eventually lowers demand for new housing, and prices would fall to reach an equilibrium. The second reason we believe today’s high inflation numbers are likely to be transitory is because it coincides with our understanding that we are experiencing a cyclical inflation phenomenon rather than a secular one. Secular factors such as an aging demographic, technology-enabled disruption, high government debt to GDP, and globalization trends that have dominated our economy over the last decades and are generally disinflationary, making a resurgence of near-term inflation due to secular forces highly unlikely. Additionally, bond markets also appear to be discounting inflationary risks, with 10 and 30-year yields declining 24 and 28 basis points respectively over the most recent quarter.

Although we question the sustainability of the current levels of inflation due to factors mentioned, developments in the coming months bears monitoring, as higher than expected inflation can be disruptive for financial markets, at least in the near-term. Over the longer-term, we see secular disinflation trends to continue to dominate while government policy being the most likely driver of secular inflation, not the price of goods.

The Fed continues to have tremendous influence on inflation expectations and actual inflation. When they announced a monetary framework shift with “Average Inflation Targeting” in August 2020, it signaled that the Fed would tolerate above-average inflation above 2 percent before pre-emptively acting. This skewed inflation expectations to the upside and when markets saw early signs of inflationary pressures this year, markets expected inflation to run hotter than usual before any Fed action. However, in their recent June 2021 Fed meeting, the Fed announced that they are more concerned over inflation risks than employment slack, it reinforced that the Fed is ready to act should inflation get out of hand. As a result, higher inflation expectations quickly diminished, which reinforces the influence the central bank has on the ultimate inflation outcome.

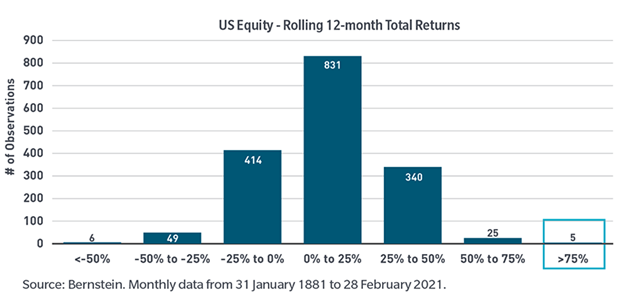

As of June 30, 2021, the S&P 500 Index have soared by over 98% since the bottom of March 2020, in what has been described as the fastest recovery in market history. To put this into perspective, markets have only experienced a 12-month rolling return of over 75% five times since 1881. Performance like this is extremely rare which consequently come with behavioral side-effects, one that is filled with skepticism over higher prices, especially during a recession recovery.

It is natural to question the sustainability of current market given where the economy was just 15 months ago. Valuation metrics ranging from the P/E to Market Cap/GDP ratios are hovering in their top quartiles while investors are sitting on a pile of massive gains. Seeing a drop in market values can be emotionally challenging given that investors are naturally loss averse. Although a correction of more than 10% becomes more likely as the markets continue to ascend upwards, we believe that pullbacks could be driven by some profit-taking and would likely be short-lived. Investors may view market weakness as buying opportunities, providing some backstop to the correction.

Currently, economic fundamentals are improving while corporate earnings growth are expected to remain healthy going into 2022. Combine this with a still relatively accommodative Fed, arguments can be made that market prices still have room to run. Additionally, there are still segments of the market that remain attractive, supported by strong secular tailwinds. We assert that today’s environment is beneficial to be selective, where we are not invested in the stock market, but a market of stocks.

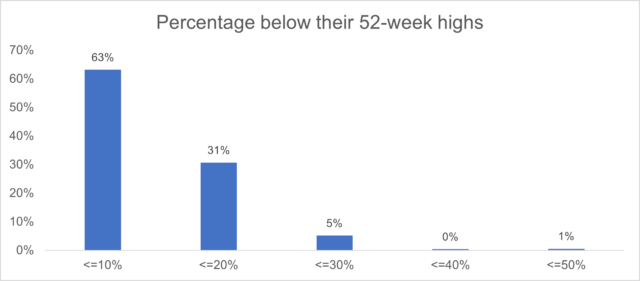

There is still over one-third of companies in the S&P 500 that are trading at more than 10% below their 52-week high. Long-term investors could use potential volatility in the future and selectiveness to create buying opportunities.

What is counterintuitive is that markets may want investors to have concerns at any given time. The time where investors should be most worried is when there are no market concerns whatsoever. The fact that market over-valuation is on the minds of investors provide signals that market exuberance may not be as frothy, de-risking the potential of a bear market driven by market excess.

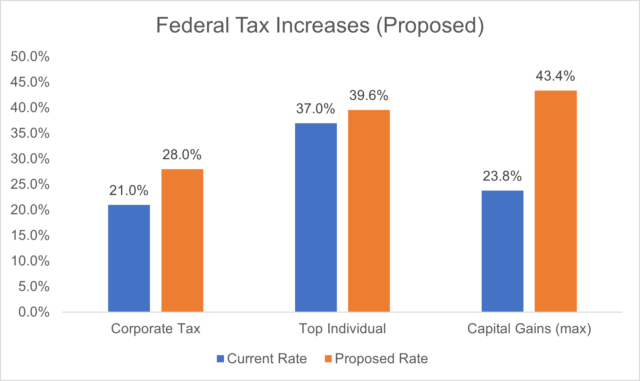

To pay for additional spending packages announced by the Biden administration, legislation to rewrite part of the tax code has been proposed as a means of funding those packages. Items that are part of the proposal include to increasing the marginal corporate tax rate from 21% to 28%, a minimum 15% tax on corporate book income, an increase to the top bracket individual rate, additional payroll taxes for employers and highly paid employees, a shift in the maximum capital gains rate to that of the individual rate, and the elimination of step-up in basis treatment on inherited assets. Although these provisions and rates are up for negotiations, they still make a significant impact for investors to take notice.

Despite potential negative effects from increased taxes on economic growth (should the current provision and rates pass as proposed), economic growth continues to be supported by other favorable factors that would keep production along its longer-term trend. Markets will likely experience an adverse knee-jerk reaction to any developments that suggest higher taxes are on the horizon, but we believe corporations and consumers will continue to create, adapt, and innovate in a free enterprise market. The political battle will probably heat up over the months ahead on the size of additional spending packages and how to fund them.