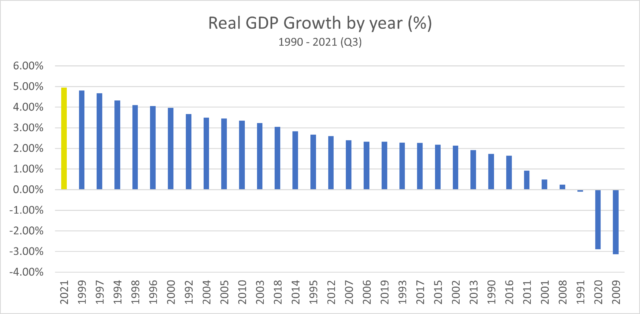

It was a year of no comparisons in economic data in 2021. Economic data faced massive “base effects” in 2021, where year-over-year increases for inflation and other metrics appeared large in comparison to the weak prints at the beginning of the pandemic in 2020. Abnormality of markets made comparing several economic metrics relative to pre-pandemic levels extremely difficult in understanding whether strong data is indicative of a new cycle or simply a temporary boost coming out of the pandemic. The first two quarters of economic activity, measured by real GDP, expanded at a healthy pace of 6.3% in Q1 and 6.7% in Q2. Economic activity however began to shift at the beginning of summer when the Delta variant was discovered and lockdown anxieties re-surfaced. Real GDP in the 3rd quarter only increased by 2.3%, much below what was initially projected at the first half of the year. Nonetheless, the general economy is still on pace to have its best real GDP growth in over 30 years.

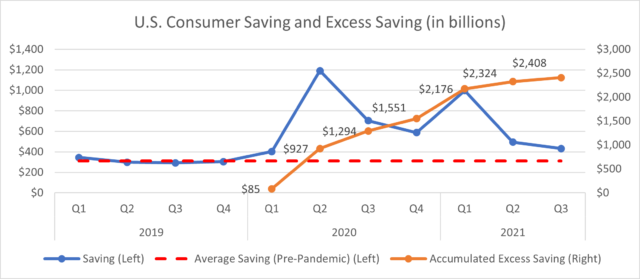

Large fiscal stimulus combined with record levels of household savings created an ideal environment for robust consumer activity that drove economic growth in 2021. U.S. consumers account for 70% of GDP contribution, which creates an outsized influence on the direction of the economy. Heading in to 2022, U.S. consumers sit on about $2.4 trillion in excess savings, accumulated from the start of the pandemic. That’s about 13% of GDP that could be supportive of continued pent-up demand from consumers. However, persistently strong inflation numbers in 2022 should be monitored closely, primarily on how it may impact consumer confidence and consumption activity.

Consumer confidence remains strong today, which is reflective in a lofty number of people quitting their jobs each month: over 4 million since July 2021. The labor market is tight with over 10 million job openings and a 3.9% unemployment rate as of December 2021. Exacerbating challenges in an already tight labor market is that the labor force participation rate continues to remain stubbornly low at 61.90%- which according to the most recent Fed’s minutes, is preventing the central bank from labelling the labor market as full employment. Several reasons such as greater share of baby boomers’ retiring (leaving the workforce altogether), increased childcare requirements at home due to Covid, labor force skill gaps, and discouraged workers among others could be keeping the labor force participation rate low. This can be significant because there is no quick fix to this issue and a tight labor market is already causing wage pressures across the economy, which could lead to further wage pressures and inflation.

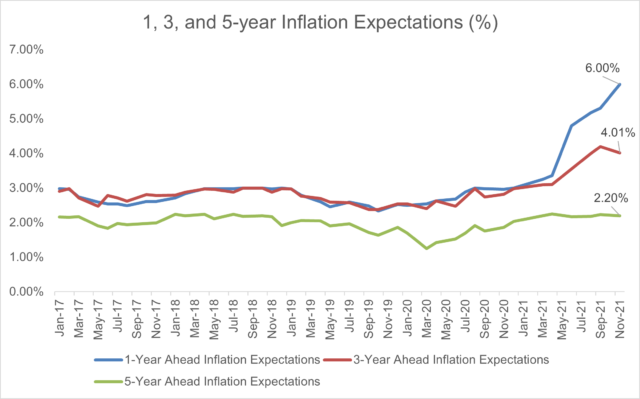

Fears of persistently higher inflation has been a buzzword and topic of conversation throughout 2021. This have shifted short-term inflation expectations upward as markets now expects one-year ahead inflation to be approximately 6%.

Inflation expectations could be a more important indicator to observe than actual inflation itself because actual inflation often is self-manifested by its own expectations. If inflation expectations get out of control, it becomes extremely difficult to maintain price stability in the economy. For that reason, the Federal Reserve wants long-run inflation expectations to be anchored at 2% and to protect its credibility of its inflation objective. The best way to accomplish this is to let the market know that inflation is under control, and no hesitations will be made to combat it, if necessary. So far, it appears that the Fed has achieved anchoring long-run inflation at 2% based on the markets’ forward 5-year inflation expectations. From a policy standpoint, finishing its quantitative easing program early and signaling confidence to combat monetary inflation through rate hikes have been effective thus far.

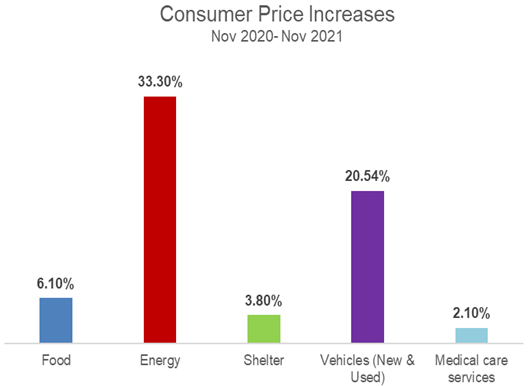

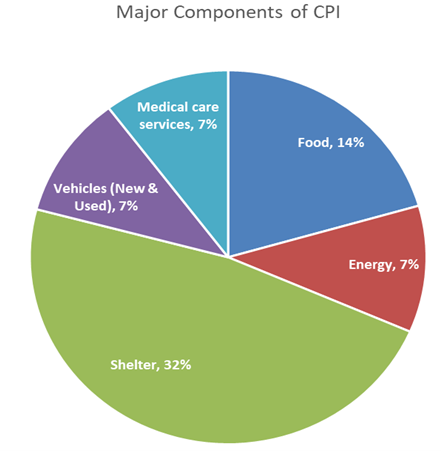

The one wild card for potentially higher inflation in 2022 is shelter cost. The biggest component of the Consumer Price Index (CPI) basket is shelter (32%), which has been relatively muted (3.8% YoY), despite national home prices registering double digit YoY growth since the beginning of last year. The latest reading was a 19% increase in October 2021, based on the Case-Shiller National Home Price Index.

The outsized influence the shelter component has on headline inflation numbers should be monitored closely. According to the study by the Dallas FED, there is approximately a year and half lag (18 months for rent and 16 months for owners’ equivalent rent) between house price growth and shelter inflation. Therefore, rapid appreciation in housing prices should be reflected in the CPI reading by mid-2022. It could create an adverse psychological impact on consumers to see one of their wallet’s largest spending items (shelter) increase dramatically, so managing inflation on other CPI components and having a tough stand on inflation from the central bank is critical. So, how is inflation shaping up for 2022? In general, price pressures from energy and other elevated components of the CPI should ease as supply chain bottlenecks and production output return closer to normal levels; That impact might be offset by an increase in shelter inflation. However, the same base effect that made 2021 inflation look lofty, can make 2022 inflation look less elevated, making a positive psychological impact and keeping inflation expectations at bay.

The outsized influence the shelter component has on headline inflation numbers should be monitored closely. According to the study by the Dallas FED, there is approximately a year and half lag (18 months for rent and 16 months for owners’ equivalent rent) between house price growth and shelter inflation. Therefore, rapid appreciation in housing prices should be reflected in the CPI reading by mid-2022. It could create an adverse psychological impact on consumers to see one of their wallet’s largest spending items (shelter) increase dramatically, so managing inflation on other CPI components and having a tough stand on inflation from the central bank is critical. So, how is inflation shaping up for 2022? In general, price pressures from energy and other elevated components of the CPI should ease as supply chain bottlenecks and production output return closer to normal levels; That impact might be offset by an increase in shelter inflation. However, the same base effect that made 2021 inflation look lofty, can make 2022 inflation look less elevated, making a positive psychological impact and keeping inflation expectations at bay.

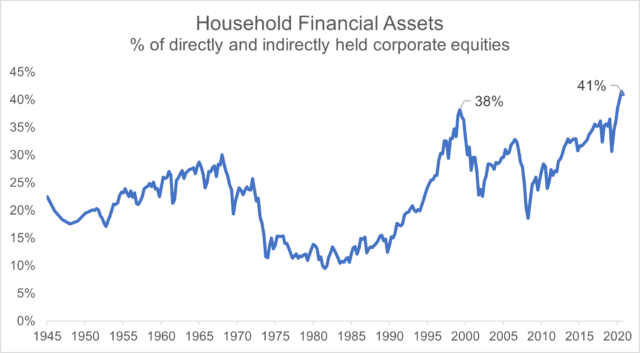

Investors poured records amount of money into the stock market last year driven by a combination of cheap money, strong economy, frenzied retail trading, and a lack of other attractive investment options. Overall US household wealth reached a record high, attributed to gains in the stock and real estate markets. According to data released by the Fed Board of Governors, equity share of financial assets have now reached a 70-year high, exceeding the level reached at the peak of the dot-com bubble.

With the Fed signaling the end of their quantitative easing program and begin to set up rate hike expectations moving forward, financial assets volatility has picked towards the end of 2021. Household wealth is primarily tied up in two things- stocks and real estate, both of which are tied to the movement and level of interest rates. Both have appreciated tremendously after interest rates decreased to record lows to fight the effects of the pandemic. The debate continues about how fast central banks will raise rates to combat inflation, and how badly it could potentially erode economic growth, sentiment, and valuation multiples.

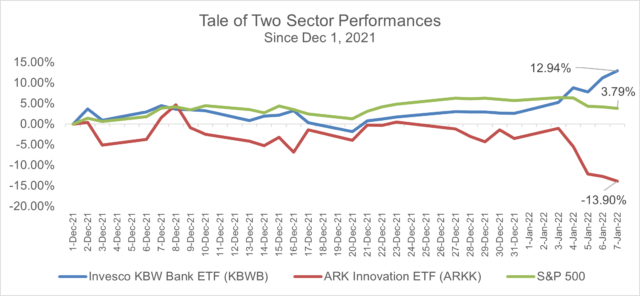

The recent bout of volatility has impacted stocks most sensitive to movement in interest rates- a stark contrast between financials (primarily banks) and non-profitable tech stocks highlights this difference.

Investors have been investing the same way over the last decade- based on falling interest rates, globalization, slow economic growth, and low inflation. Those are huge macroeconomic cycles which have benefitted large growth and tech stocks in the last decade. In fact, the combination of these factors along with the rise of passive index investing have created a large performance dispersion between the mega cap growth stocks and the rest of the market.

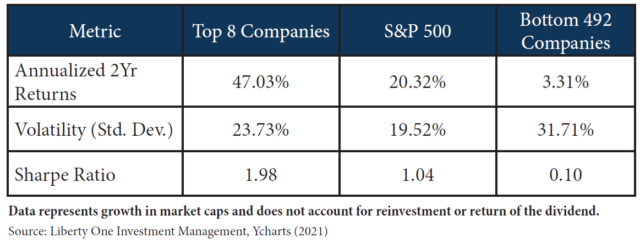

The top 8 companies in the S&P 500 significantly outperformed the index itself and the remaining 492 companies since December 31, 2019. The outsized returns of the mega-cap tech stocks were driven in part of record low interest rates and record profits harvested from the digitization of the global economy which was further fueled by the global pandemic. The overall lower volatility in the basket of the top 8 stocks have also been supported by technical price support from asset flows, and buying the dip behaviors from investors, especially into passive index funds and the mega-cap stocks. Passive index funds amplify the technical price support for mega-cap stocks because the largest companies receive the highest asset flows due to the index’s market cap weighted nature. The adage of money grows where money flows is anecdotally evident within passive funds, where the largest companies receive the most money, not necessarily the most productive or efficient companies.

The challenge for markets moving forward is whether the patterns of past macroeconomic cycles will remain the same or will new patterns emerge and create new investing environments for the future? With the Fed signaling tighter monetary policy and Congress’ gridlock over further spending packages, could the pullback of market-friendly policies steer the market and economy astray? On the contrary, higher fiscal deficits and debt burdens could limit long-run economic growth and limit the possibilities of higher short-term rates. Global growth may also slow to its pre-pandemic long-run average which would create a “more of the same” environment over the medium term. One thing for certain is that changes are likely on the horizon and markets will have to navigate them. While we go through those changes,

In our view, vulnerabilities in the markets today should be discussed to set reasonable expectations for 2022. The prevailing sense of comfort found in solid economic data, robust earnings, accommodative policies, and lack of other attractive investment options have led to a high level of equity positioning in investors’ portfolios. Such bullishness and high levels of equity positioning could exacerbate a market reversal should one happen, potentially greater for high beta or market sensitive stocks.

Nonetheless, elevated equity positioning is usually not an effective timing tool. What it tends to do is exacerbate the rout when sentiment sours and selling begets selling. Market experts’ forecasts in 2022 is for economic growth to moderate somewhat from 2021 levels but remain in positive territory. S&P 500 companies are also expected to report a 19% increase in earnings this quarter while Covid fears and supply chain issues continues to normalize. These strengths point to a stronger buffer for markets to fundamental shocks, though crowded equity positioning could create some volatility.

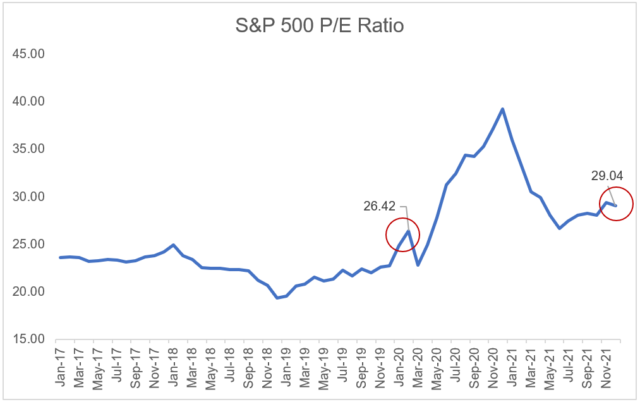

From a valuation perspective, the stock market earnings multiple is more stretched than before the pandemic crash.

Although it is still too early to predict how corporate earnings will shape up in 2022 and what kind of impacts higher rates will have on multiples, a higher starting multiple has historically resulted lower future stock returns and potential vulnerabilities to higher-than-expected interest rate environments. It is therefore prudent for investors to understand their existing risk exposures and manage their portfolios with appropriate risk diversification. Such can be achieved by not only diversifying “across” asset classes, but also “within” a single asset class category. 2022 is shaping up to be a year of potential major market shifts, and investors are encouraged to position themselves to navigate the perils and opportunities that are likely coming their way.